One of the great joys for me of this time of the year is finally being able to catch up on some reading. I’ve spent the last week going through reports, articles, and podcasts I’d been meaning to dive into for a while.

Here’s my reflection on where we are as we go into 2026.

1. Alcohol and the era of moderation

The IWSR recently published a report on drinking that did the rounds. There were two charts that showed the story.

First, is the absolute chart that reveals that Brits are now on a par with Americans for amount of alcohol drunk per capita each week.

There is a clear decline within the UK down to just over 10 drinks per week on average.

Gen Z’s role is shifting

The common narrative for a long time was it was Gen Z leading this charge, but data from summer showed that trend is bucking.

“Recent data has shown the proportion of gen Z – those born roughly between 1997 and 2012 – who are of legal drinking age and have consumed alcohol in the past six months has increased by 7% between 2024 and 2025.”

Source: Guardian

In fact, as that article suggests, a lot of Gen Z’s prior teetotalism can be accounted for being underage, unemployed or in less stable working environments generally. The generation is older, working and more affluent than they were in previous years.

And so overall declines in drinking in the UK must be broader.

Let’s look at that IWSR data again, but indexed rebased to 1990.

The shape of this chart got me digging into a few other thoughts of what correlates at this time.

A few key thoughts here:

There’s a clear financial crash change around 2007-2010 that correlated with the downward trend

Drinking rose throughout the 90s and peaked in early 2010s (just as I and other millennials starting drinking)

I was interested in how this correlated to public sentiment towards politics – whether the New Labour optimism was fuelling it.

What this means for brands

There’s a decline in drinking for sure, but it’s not as clear cut generationally as once thought. For anyone selling in the low or no alcohol space, this won’t be a surprise.

The bigger questions might be why this is happening. Understanding the motivations between reduced alcohol will help shape why and how to sell to someone.

2. GLP-1 users are the new happy, premium consumers

GLP-1s are tricky beasts.

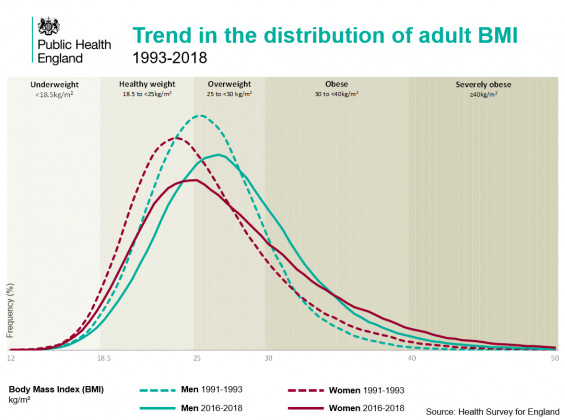

When I think of GLP-1s, my default is to think more of toxic culture of skinniness than it is to think of overweight people creating better relationships with their bodies.

I know statistically that isn’t correct. In the UK, the distribution of of weight leans far more to the overweight and obese end.

And when we look at global trends the picture is clear too:

Obesity is on the rise, and most sharply in the faster-growing middle income economies.

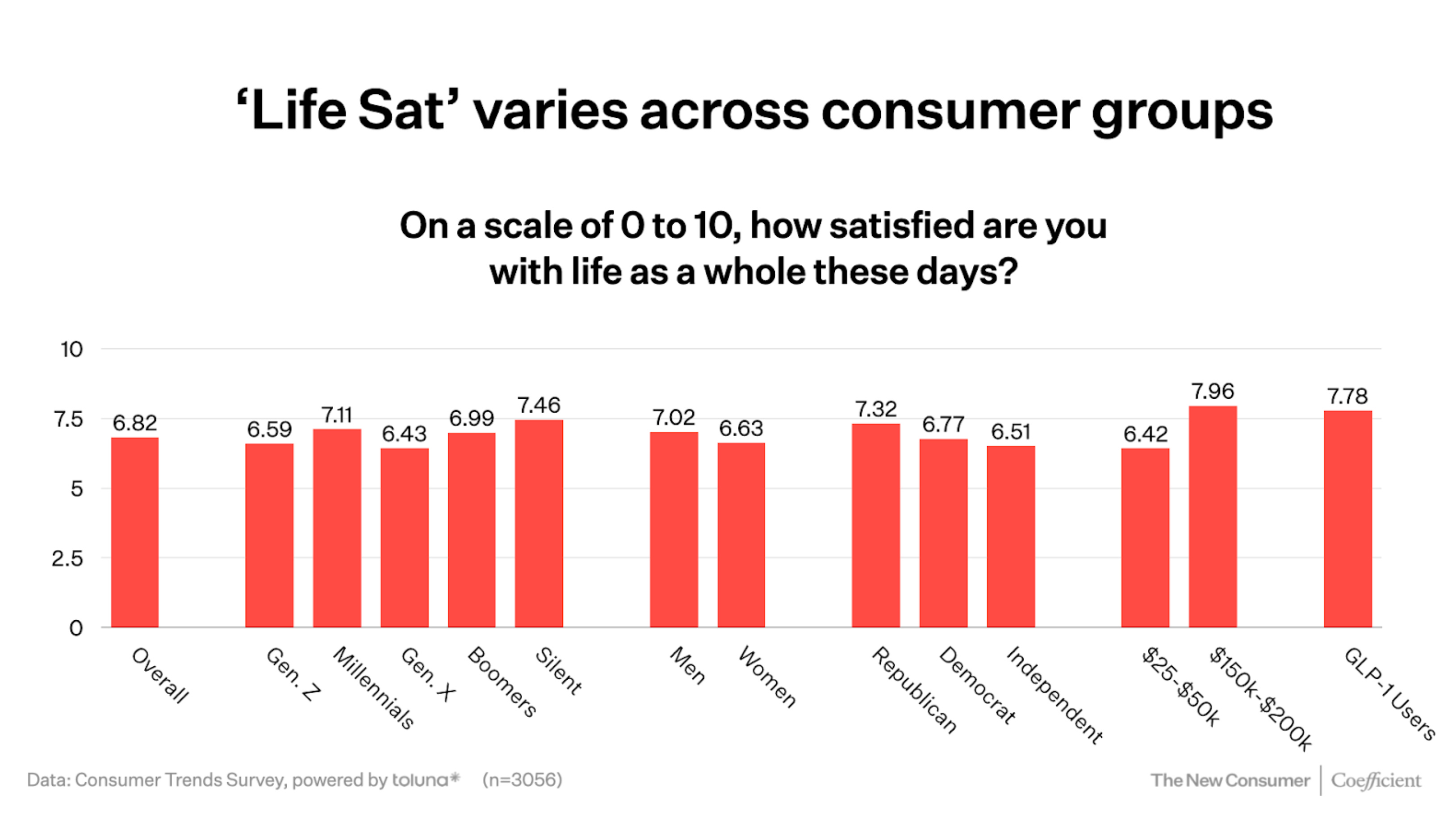

So this set of stats is interesting from the New Consumer report.

Life satisfaction is 14% higher for GLP-1 users than the average. And in fact is one of the best predictors for life satisfaction – second only to those who earn $150-200k/year.

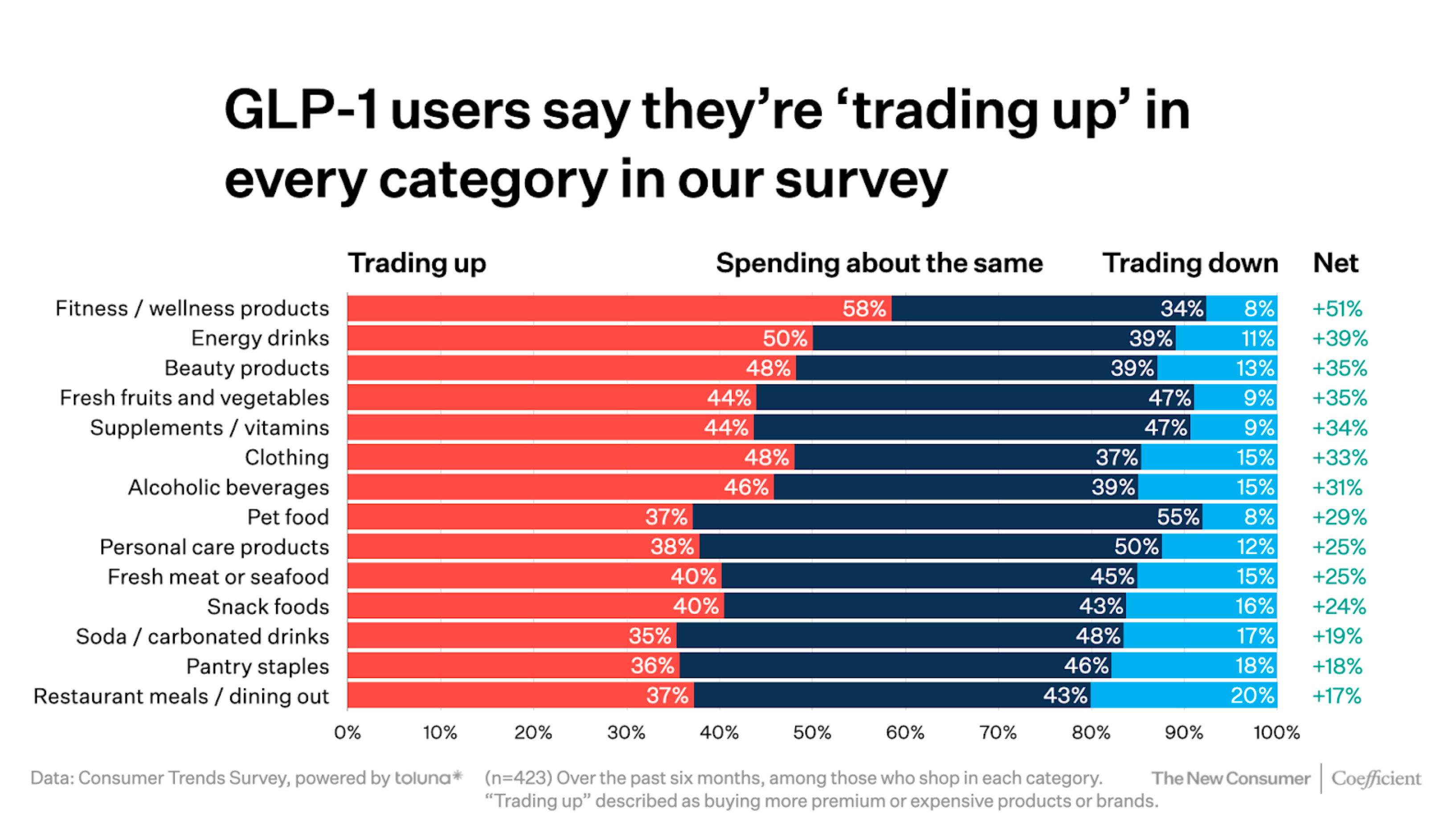

Most interestingly for brands is what that increased life satisfaction correlates to in spending power.

Unlike the general population, where there is a mixture of trading up and down depending on category, GLP-1 users are almost trading up in every category from the Coefficient Capital survey.

Perhaps the surprising ones are in restaurant meals (17% up), and snack foods (24% up). But as their report also states a lot of this interest will come from new brands or products specifically catering for them.

3. Drug use on the rise

While alcohol make be down, and low and no down with it, lots of drug use is on the rise.

18.1% of British 16-24 year olds have taken an illegal drug in the last year, which when you consider the 39% who never drink, might offer part of the picture.

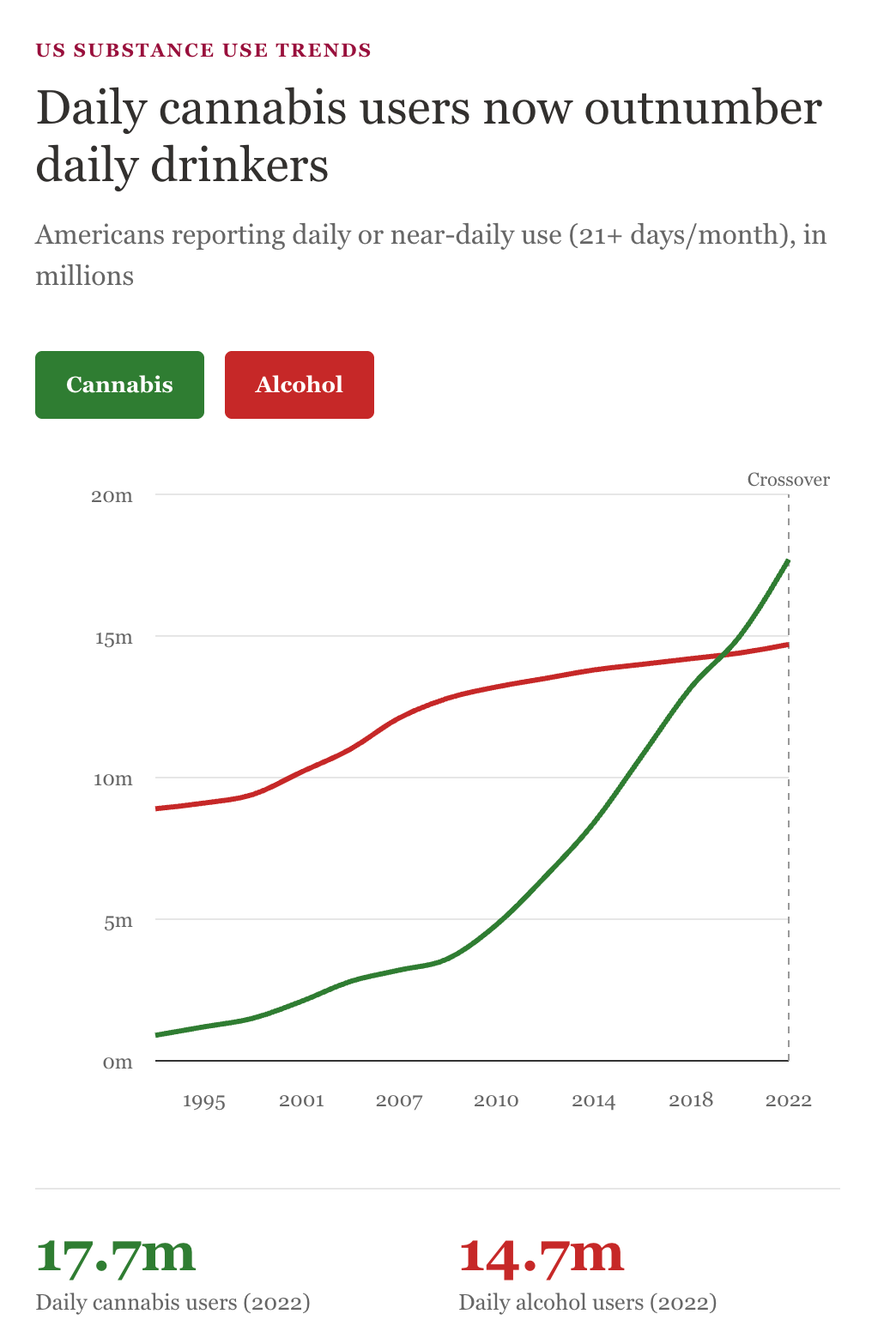

In the US, while daily alcohol drinkers are flat or showing slow growth, daily cannabis users overtook drinkers a few years ago.

Meanwhile, lifetime use of cocaine has doubled since 2001 at a time when regular drinking has declined significantly. The overall numbers are still far apart, but the relative trend is clear.

It is too simple to look at alcohol moderation and say that society is moderating. For some, it is definitely about blanket moderation, but for others one drug is being swapped for another. And in many cases, some of those swaps will be worse rather than better.

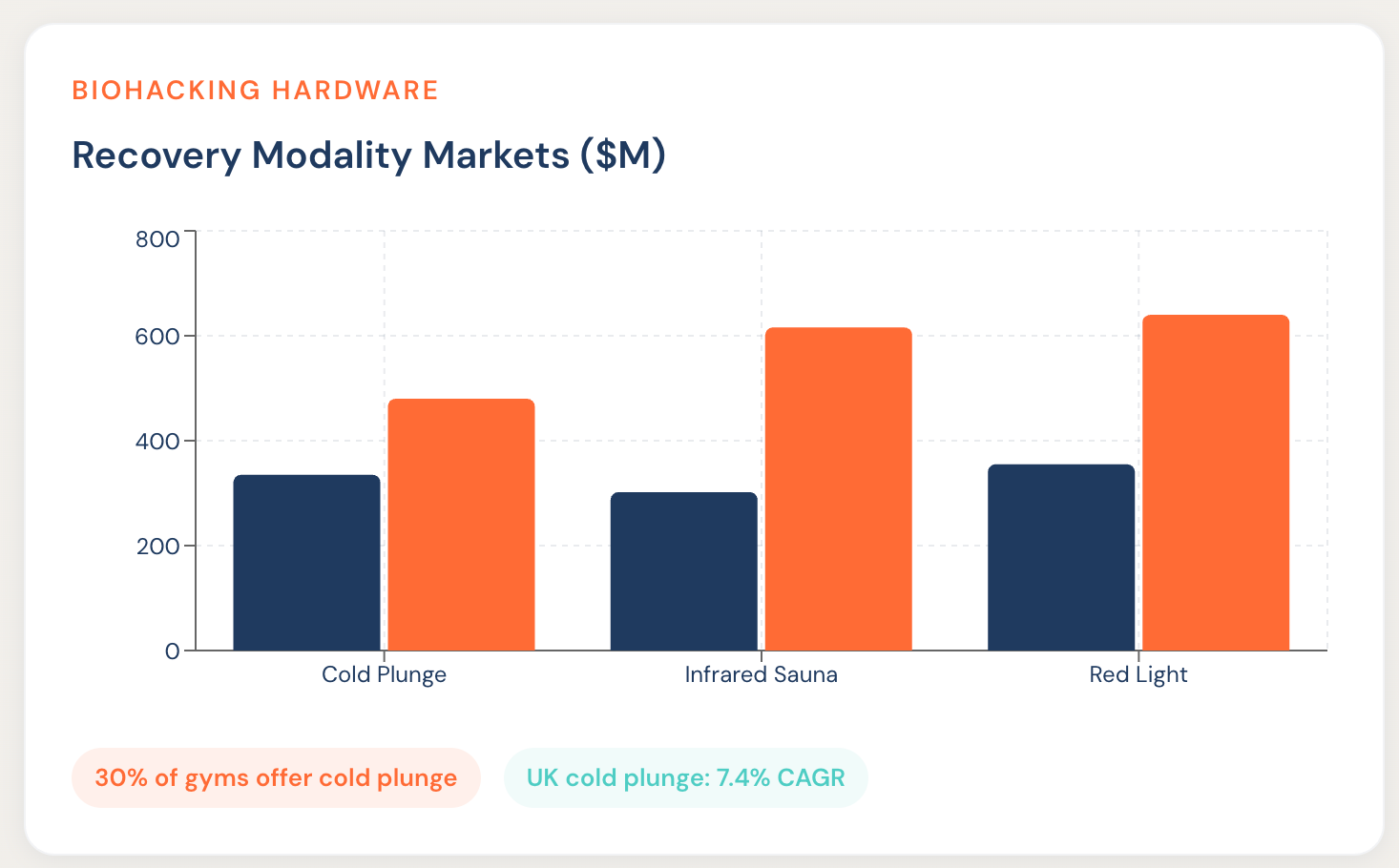

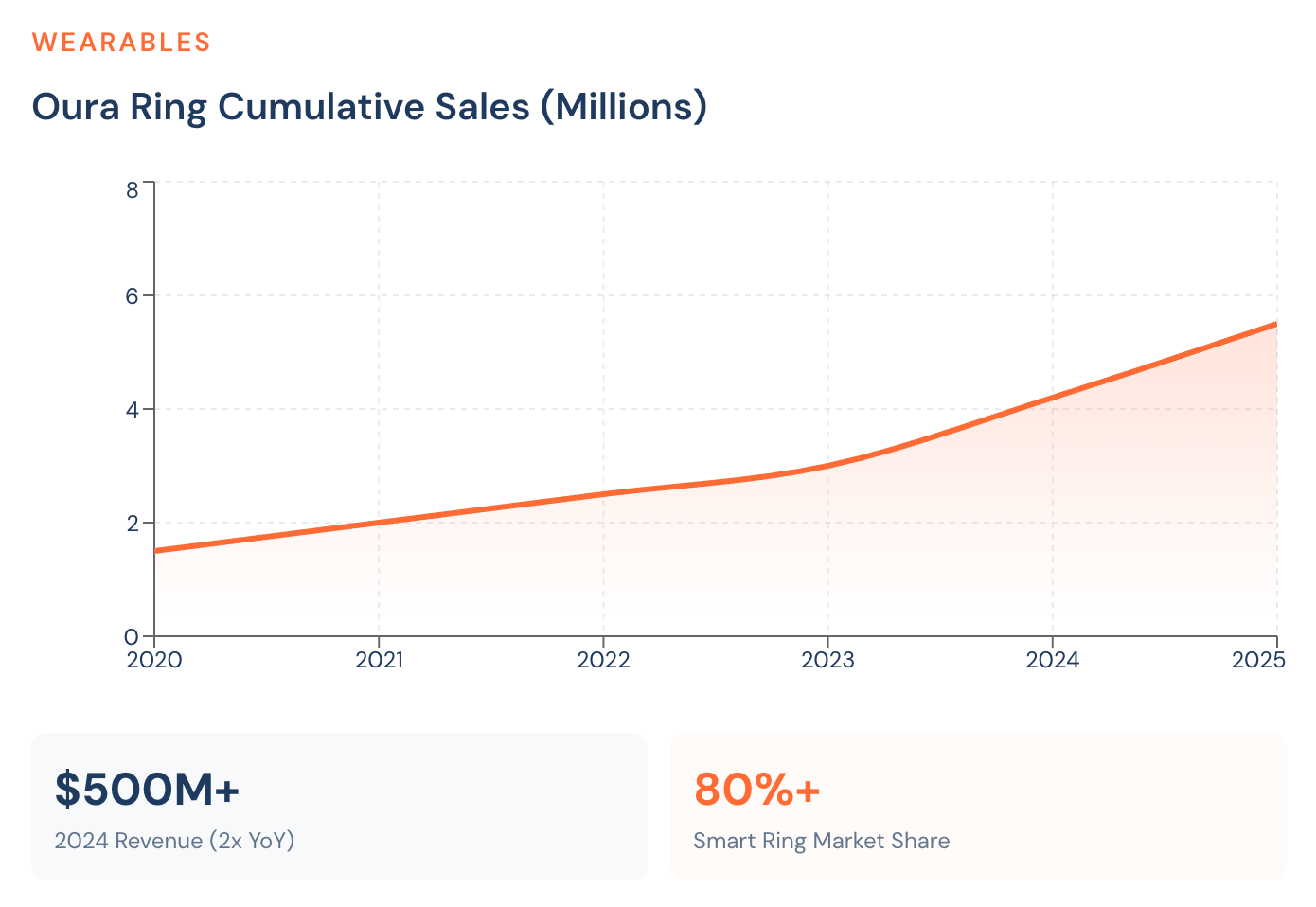

4. Longevity is on the rise

2025 started with the Don’t Die doc landing on Netflix. At the time, everyone laughed.

Today, the laughter seems to have quieted down.

Lots of biohacking is expected to rise.

Oura Ring sales have close to tripled in five years.

£200m is being spent on anti-ageing in the UK.

I had an IV in early December, and part of that was a NAD shot. NAD is still expensive to get as an injection or home shot. Most packages you’re looking at £300+ per month to properly get the benefits.

The number of people who will spend £3,600 per year on this is low. But this is the tip of the iceberg for the market.

5. Comms & storytelling is more important than ever

My old boss, colleague, board member Peter Sigrist used to consistently extol the value of storytelling. Whether it was in corporate comms, education, politics, or now quantum computing, I’ve never heard someone so stalwartly defend the value of being able to communicate a narrative.

Turns out the world is waking up to Peter’s worldview.

This year, we saw all the big AI companies invest heavily in storytelling, comms-focused content positions. It caused a few eyerolls given what these companies are doing for broader content around the world.

But as this WSJ article reinforced, it’s never been as important to find storytellers in the world. Source.

The number of roles including the word storyteller have doubled year over year.

This isn’t just marketing, companies want specific storytelling skillsets

Continuing trend of owning your own content distribution

Huge salaries to go with it

In advertising, this is important too, but while adverts try to capture attention in nano-seconds, this feels like the longer sell once you get someone into your world.

6. Confidence in consumer investing is back

Sugar Capital, the venture arm from the POPSUGAR founders, posted a call to arms in early December with their post “The Golden Age of Consumer Investing.”

I read Brian Sugar’s post enthusiastically.

“A gummy vitamin company reaching $300 million in revenue on $20 million of primary capital. Contribution margins above 40 percent. Meaningful EBITDA before the Series B.”

“Product-market fit” is bandied around a lot in startup folk lore. I know it because I had my own startup fail without it. But so much discourse around PMF is focused on enterprise, b2b, and proper tech companies. You have comments referring to how sticky user engagement is or what your DAUMAU ratio needs to be. And how to solve it is focused on switching product categories or strategies with winners the likes of Twitch, Instagram, Notion, or in the UK more recently Fyxer.

But a lot of PMF discourse doesn’t talk to consumer non-tech problems.

At Ballpoint this year, we’ve worked with over 50 brands, and I’ve audited maybe another 150. We see up close and personal the companies that:

Don’t have PMF and is unachievable unless something massive happens

Do have signs of PMF, but haven’t worked out how to scale a growth engine yet

They have it, they’re scaling, but want to push harder because they’re in a growing category and need to be dominant

When Brian talks about contribution margins and ebitda, this is not an outcome of modern consumer PMF – it’s a part of it. PMF is about sustainable business models and huge accelerated growth opportunities. You need to a path to $200m and you need 30%+ CM.

Health is the focus

It’s unsurprising perhaps that this post has focused so much on health. Brian puts down this new wave of optimism to health specifically.

“Something shifted in American consumption over the past five years. People read labels. They actively avoid the processed food that built the twentieth century’s largest companies. Ozempic and its cousins rewired how America thinks about what it puts in its body.”

We share Sugar Capital’s optimism and focus.

7. There’s still scepticism in the M&A markets

Before you start pulling money from your index funds to invest in early stage consumer, there’s still some scepticism in the market.

The excellent Drew Fallon in his Substack Making Cents, posted this week the “2026 M&A Outlook.”

In it he highlighted just a few of the big issues we’re facing at the moment. Namely:

Coca-Cola are trying to get rid of Costa for $2bn having bought it for over $5bn

Waldencast are maybe selling Obagi

Estee Lauder are likely to sell off some brands

LVMH is trying to shift its 50% stake in Fenty

Nestle wants to further investment in health and is reviewing elsewhere

And the list goes on.

It wasn’t all doom & gloom, as Drew pointed out interest rates are likely to continue dropping in the US and that will be good news for all. This will particularly be true for the portfolios with lots of DTC weighting which are now approaching the end of the 8-10 year fund cycles. Expect lots of pressured dealmaking for brands in this part of the cycle.

And the areas Drew has the highest confidence in:

“Protein and fiber [sic] companies (and hydration to a lesser extent) that are gobbling up market share right now are critical assets that must be owned”

This said, however, 2025 ends with broader M&A at an all-time high with $4tn in dealmaking done this year.

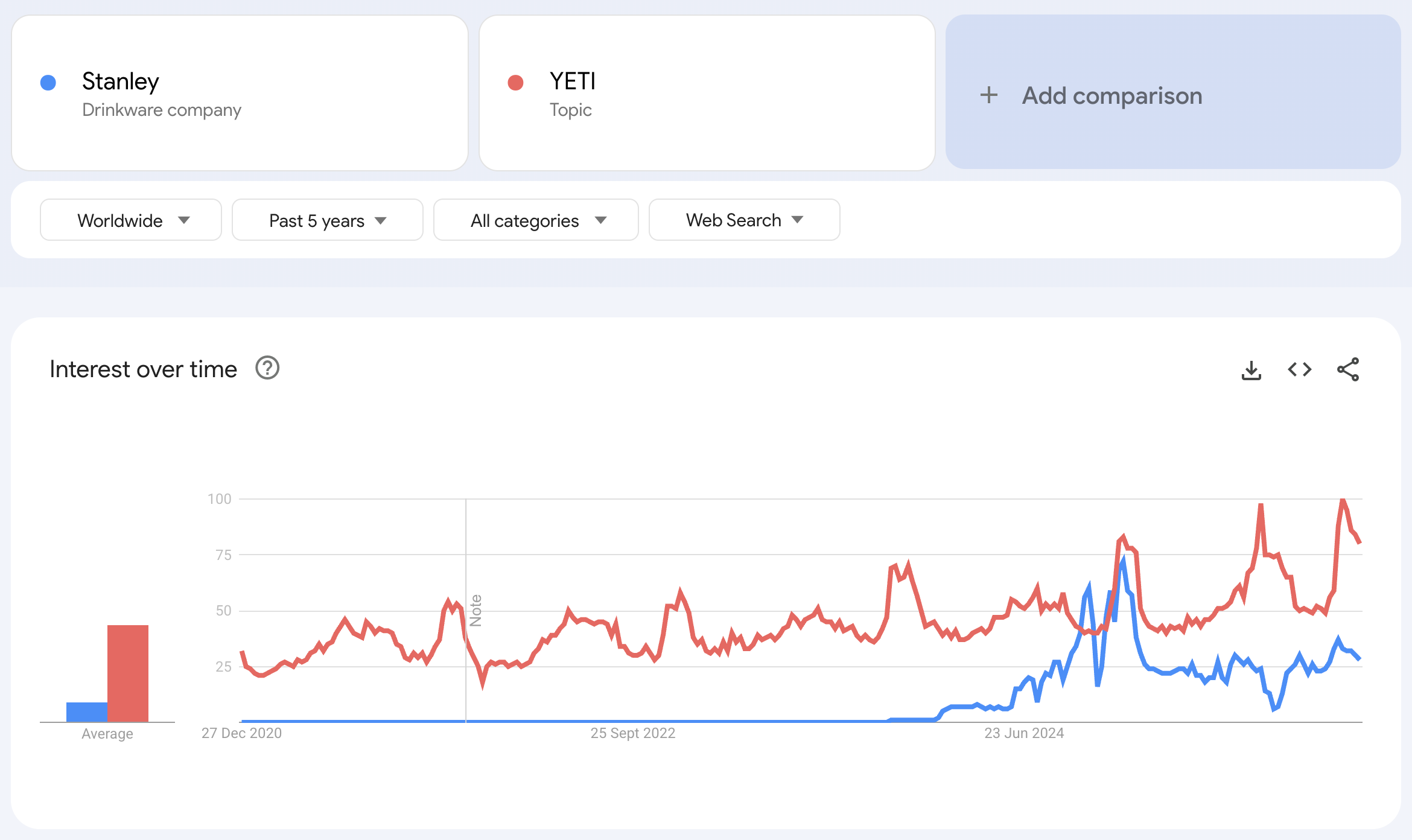

8. The two horsemen of the 8-figure world: LTV debt and Brand debt

I was reminded of Sean Frank (the Ride CEO)’s comment this month about Stanley:

Go back two years and Stanley were unavoidable. They were on every Meta ads inspo board out there. They were being case studied. And now they’re in a clearout section.

If you were YETI, who of course are broader in catalogue than Stanley were, you could have easily fallen for switching strategy. Fortunately their Google Trends data shows a slow but steady move up and to the right. They’ve remained stable and growing, while Stanley hit a hype curve they couldn’t follow back from.

We don’t know Stanley’s unit economics, but it’s a pattern we see often:

Hype doesn’t create a brand

9. Beware of category cycles

This was a great chart shared by Ben recently about category/brand growth.

One key thing jumped out for me here about how to think through strategy.

Lots of businesses I know and meet aim for contribution break-even or contribution-profitability and their goal is to scale up to that point. In early days it’s a good strategy because it helps you build up to a level of net margin profitability by building enough revenue to cover your opex.

But once you’re there, you should think about category.

Now every founder is biased towards the strength of their own category. You are after all a founder and have long term belief in it.

But trends are cyclical. Just because GLP-1s and healthy snacks are big this year, it does not mean that’s a permanent state. We’ve seen in the space of a decade the explosion and death of artificial meats. The things that were rampant for millennials are unimportant for gen z and so on.

The move towards green looked like an inevitable change for the 2010s, but there’s backlash against it now. Governments, populism, consumers are shifting and moderating.

We are in a health cycle at the moment, and so lean in to your strengths. Lean into the growth.

But also make sure that you are not creating fragility. Running at £0 net profit is better than negative. But if you’re in the position to have customer growth for the benefit of cash flow growth – and you’re in a cycle that could change – then build in some optionality.

10. The constant battle with affordability

The West seems to be battling away a recession every month. Only 42% of Brits believe they will ever be able to afford to buy a house. 56% of Brits say they’re impacted by the cost of living crisis this year.

Amongst young people, it’s the single biggest issue affecting the country. More than seven million people in the UK are going each month without essentials.

And amongst the highest earners, tax rates plus loss of child benefit mean that if you’re earning £125k per year, you’re actually worse off than earning £99k per year.

There is a higher number than ever who forgo basic necessities. There is a growing middle who who without support from Bank of Mum and Dad can’t afford housing. And the country’s best earners are disincentivised to earn more.

The ongoing joke about millennials is if they ditched flat whites, they’d be able to afford housing. Except for many, all that saving in the world won’t get them on the ladder. For them, buying premium makes sense.

There is of course lots to be optimistic about in the economy. But it’s also important that brands really think seriously about what type of company they are. Who they appeal to.

Are you really a mass market product? Or are you super premium? Does your growth and ambition support your customer?

And equally important are you actually talking to your customer in the right way? How you speak to middle England Facebook 50+ people is not how you speak to Real Housewives of Clapton London.

Closing thoughts

The world feels more mixed than ever. Some macro signals are noisy and potentially worrying: ongoing affordability crisis, M&A scepticism, category cycles that could turn at any moment. On the flipsde, certain classes of consumer are spending more than ever in newfound categories, giving an opening to new types of brands.

Health, longevity, and alcohol moderation are certainly all singing in unison. But it’s not universal – THC products in the US continue to be prominent, and illict drug use is on the up in some categories as well. Not everyone is following the Bryan Johnston playbook quite yet.

Whatever type of consumer business you’re building, profitability remains king. Strong and early contribution margin is vital, but building net profit growth into your business is what is going to make M&A accessible.

The best founders and teams I’ve spoken to this year are all building optionality. They’re not content with cheap acquisition costs or break-even CM, they’re focusing on LTV debt and building cash into the business. Profitable enough to survive a downturn. Ambitious enough to lean into growth when the window opens. And perhaps most importantly, more realistic about who their actual customer is than ever.

If I was the founder of a growth business at the moment, I’d be using 2026 to think about ebitda profitability rather than fragile 100% growth maximisation.

We’re not in a universally good time, but for certain sectors it certainly feels like it.

Crazy how profitable selling health is. The irony is that most people can have health without spending a dime. Curious how long it takes for the market to price MB=MC.