2026: Part 2

With gloominess ahead, we can borrow from the past to predict who wins this year

At the end of December I reflected on the year ahead and some key trends I’d collated, seen, and thought were useful to our clients. That turned into one of the most shared and read posts of the year.

Today, I’m back with a reflection on where we are today.

What’s stopping our growth?

This is the age old question. And usually for growth stage businesses, the answer lies somewhere in either product or marketing.

But perhaps the biggest factor is the one that we can’t control: the macro environment we all exist in.

We get glimpses of the macro as an agency when we analyse internal trends across £1.5-2m of ad spend each month. But sampling data like this is only part of a picture and is often more swayed by a particular strategy being deployed at any given time.

A lot has changed since the start of the year

This year has seen some pretty momentous change.

AI is now ubiquitous and we’re starting to see the real life impact of it, rather than the hypothetical (and this is before we get into future models).

But perhaps more immediately and tangibly impactful is the war in the Middle East.

Today’s post analyses a handful of sources including:

Think tank releases

Articles I’ve been reading the last few months from the Economist, FT etc

Google Search Trends Reports

Reddit

For most brands we work with, Q2 is a strong quarter that precedes the year’s weakest quarter, Q3. If I could predict the future, I’d be a rich man, but there’s still quite a few things I’ve seen so far that seem worth talking about.

Because I imagine this stuff will be having an impact for all of us in the coming months.

Josh

29% of UK workers admit they’ve sabotaged AI tools at work

52% say AI threatens their job.

TUC: 51% of the UK public concerned, rising to 62% for 25 to 34 year olds.

29% of UK workers admit they’ve sabotaged AI tools at work, growing to 44% for Gen Z.

The TUC finds 51% of the UK public concerned1, rising to 62% among 25 to 34 year olds.

There are hundreds of threads discussing AI anxiety in the last 30 days alone.

You won’t find this in Google Trends: searches related to “AI replacing jobs” have faded since April 2025. But ChatGPT usage in the UK tripled last year2.

Mortgage renewal, tax drag, and AI fear are hitting millennials at once

1.8m mortgage renewals

£1,018/yr from frozen tax bands

1.8 million mortgages expire this year into higher rates.

Frozen tax bands cost a £55k earner over £1,000 a year. And 52% of workers believe AI threatens their job.

On r/UKJobs, a 43-year-old on £50k described weighing a £27k offer.

On r/HousingUK, a first-time buyer watched their monthly payment jump £450 mid-conveyancing. No single dataset proves all three pressures act together. But the Reddit threads tell the same story from different angles: 30-to-45 year olds are absorbing rising costs, tax drag, and career uncertainty at the same time.

That’s the age group many premium DTC brands say drives their core revenue.

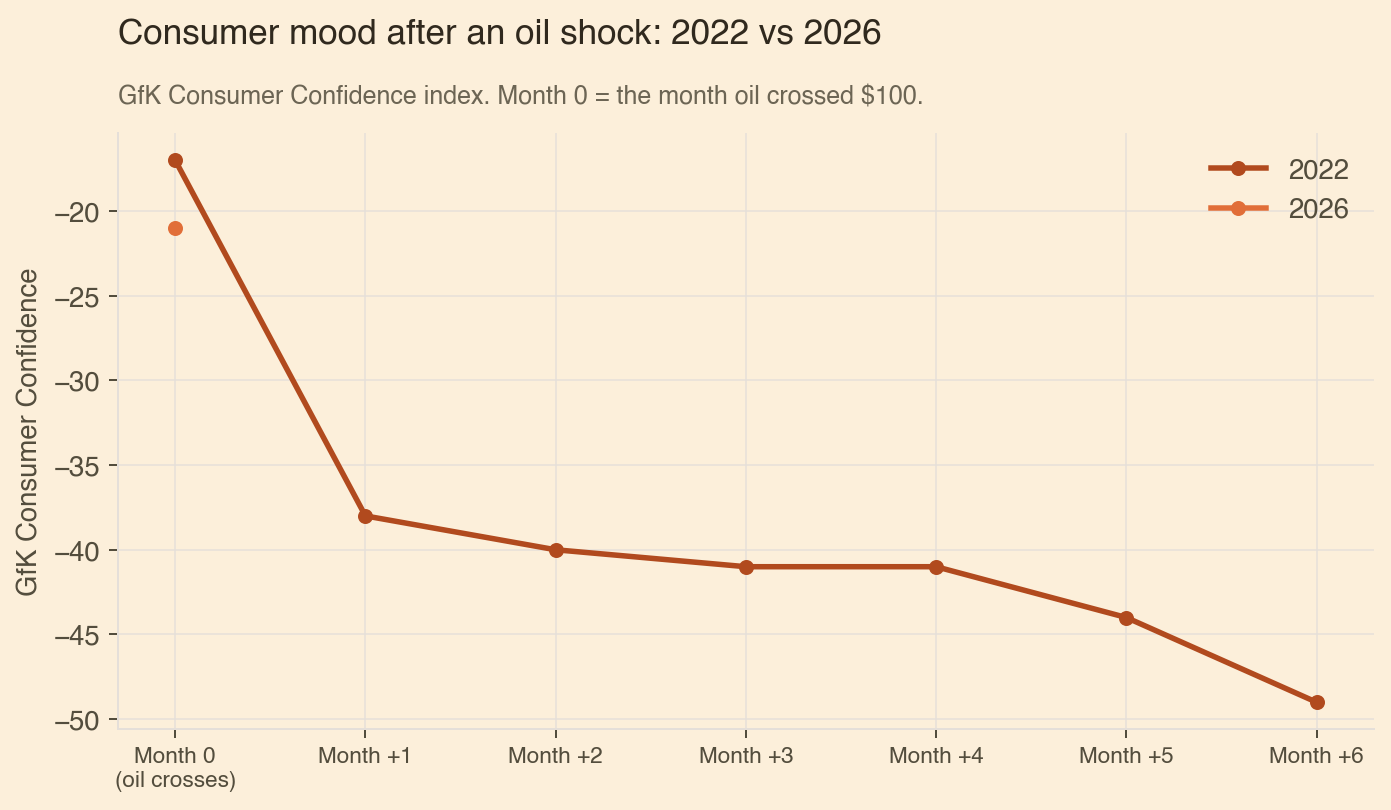

Last time oil crossed $100, consumer mood fell 21 points in a month

In March 2022, Brent crude crossed $100 after Russia invaded Ukraine. Consumer mood (measured by the GfK survey) dropped from -17 to -38 in April.

By September it hit -49, the lowest in the survey’s 50-year history. In 2026, Brent spiked to between $109 and $1133 in early April on Strait of Hormuz tensions, and consumer mood is already at -21.

The pattern is the same: oil shock, energy prices rise, mood collapses. What’s different is the starting point, and what’s layered on top.

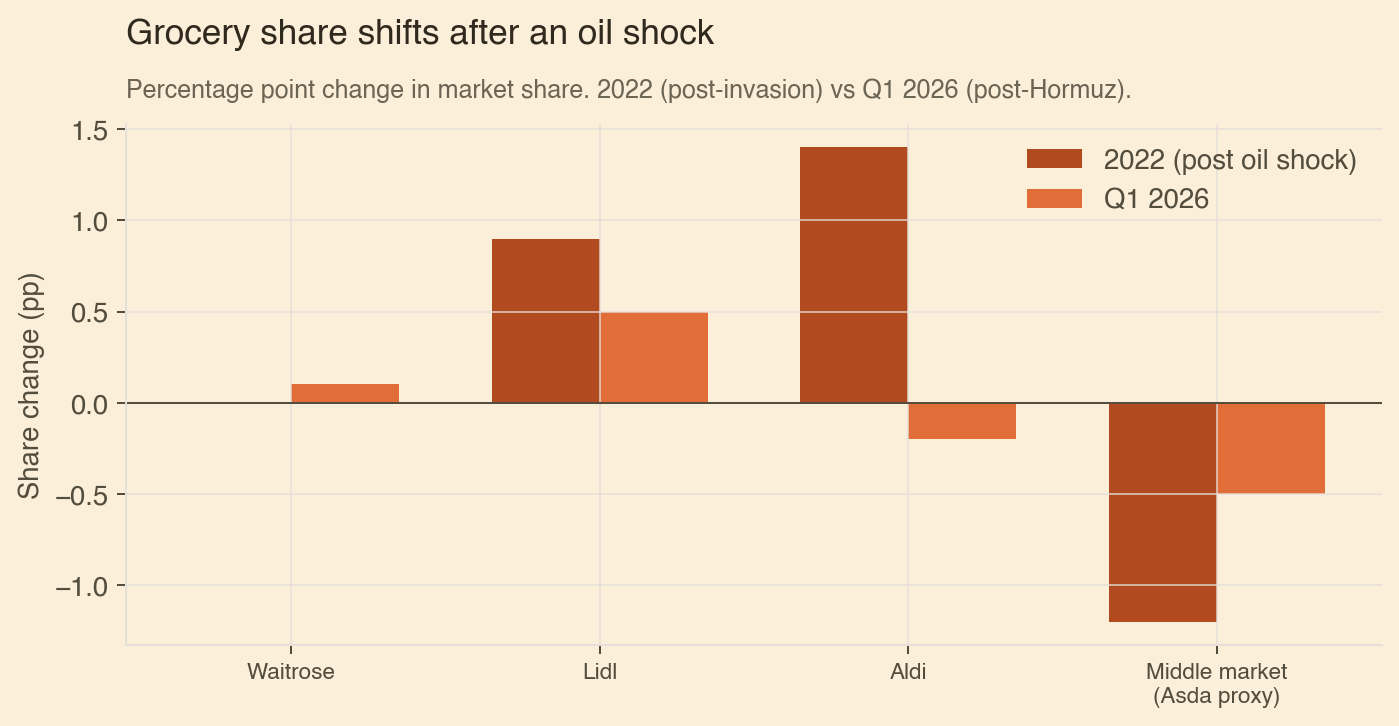

In 2022 the extremes won and the middle lost. It’s starting again.

After Brent crossed $100 in 2022, Aldi gained 1.4 percentage points of grocery share in 12 months.

Combined with Lidl, discounters grew 25% year on year against a market growing 7.6%.

Premium brands held.

In 2026, the same pattern is forming: Lidl is up 9.6%, Waitrose up 5.8%, Asda down 0.9%4.

If the 2022 pattern repeats, the middle loses the most share over the coming quarters. But there’s a difference this time: people are also dealing with AI job anxiety and a wall of mortgage renewals that didn’t exist in 2022.

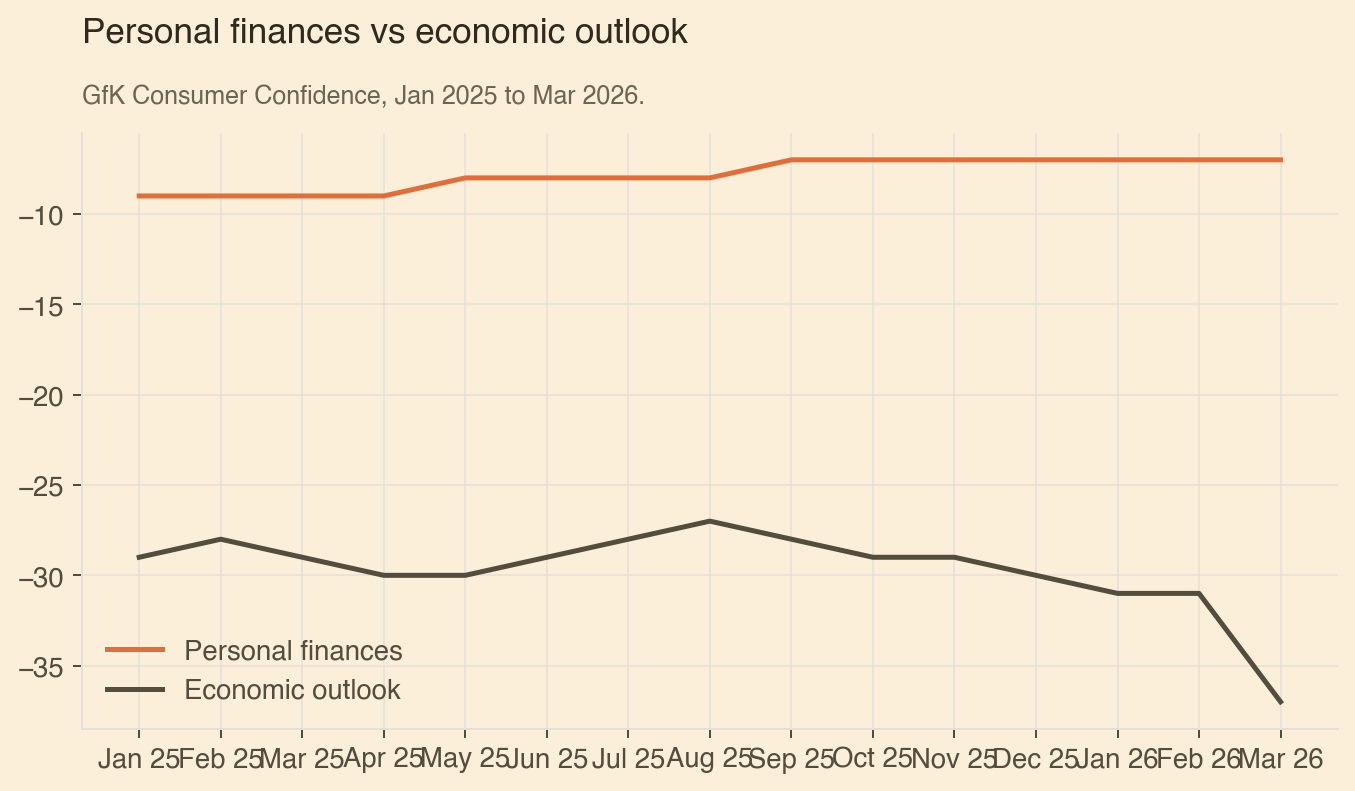

People feel fine personally but are terrified about the economy

The UK’s main consumer-mood survey, run by GfK, asks two different questions.

How do you feel about your own finances?

And how do you feel about the economy?

The answers are diverging sharply.

The personal finances score sits at -7. Not great, but stable.

The economic outlook score collapsed to -37 in March, down 6 points in a single month and 8 points worse than March 2025.

That 30-point gap is the story. People aren’t struggling. They’re bracing. And bracing shoppers don’t stop spending entirely, they just get harder to convert.

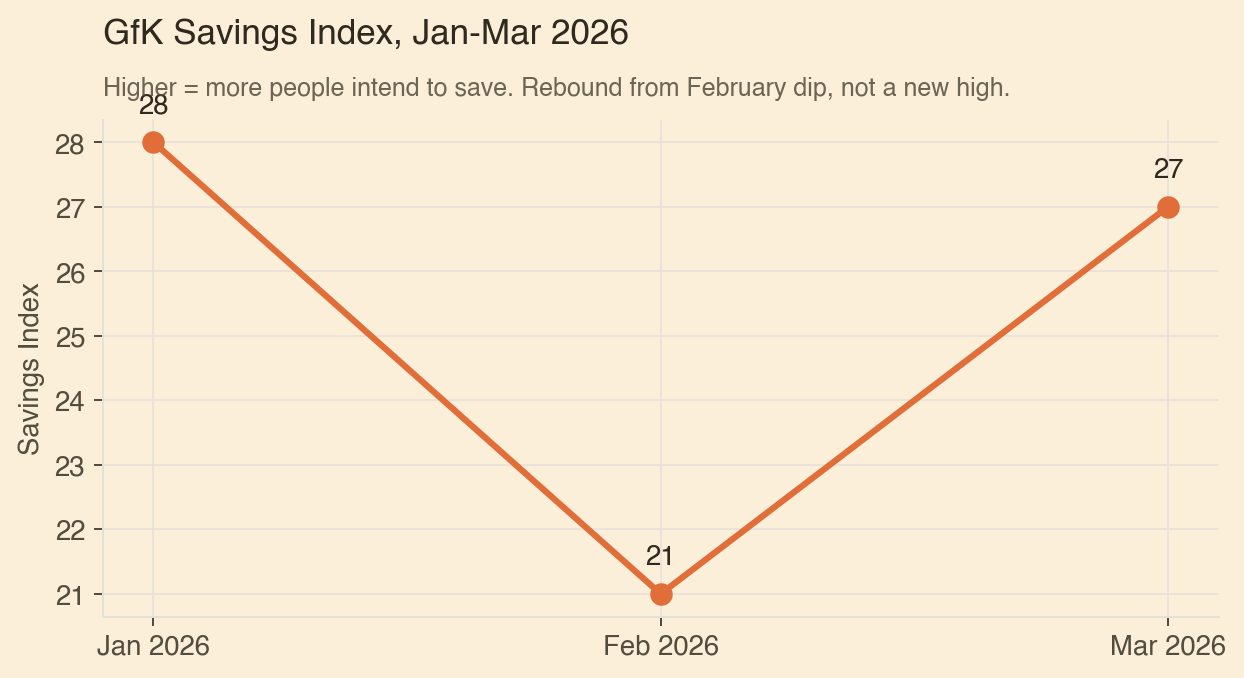

People are saving more and spending less on big purchases

The GfK Savings Index rose 6 points in March to 27, the highest reading since January’s peak of 28. Context matters: it was 28 in January, fell sharply to 21 in February, then rebounded. So this is a recovery, not a breakout.

But GfK’s own consumer insights director put it plainly:

“the decline in purchasing intentions, coupled with a six-point rise in the Savings Index, indicates people are holding on to their money and avoiding making major purchases.”

When people start saving instead of spending, brands need to earn the conversion harder.--

Health and beauty spending is up 6-8% while everything else flatlines

Note that this is February data and doesn’t capture most recent changes.

Barclaycard’s February data shows health and beauty up 6.4%, following 8.0% in January5.

Digital subscriptions grew 12.2%.

Entertainment grew 9.9%.

On the other side: household goods fell 2.9%, electronics fell 5.8%, airlines dropped 6.9%.

Overall spending grew just 1.0%, well below inflation of 3.2%.

People are choosing where to spend, and health is winning. Worth noting: this is February data, before the Strait of Hormuz oil shock.

Health and beauty was the most resilient category going into that shock, which is exactly the category you want to be in coming out of one. That resilience held through the oil spike. UK searches for strength training and gym memberships kept rising through March and early April, even as Brent crossed $100. Wellness isn’t a line item people cut first when the news gets worse.

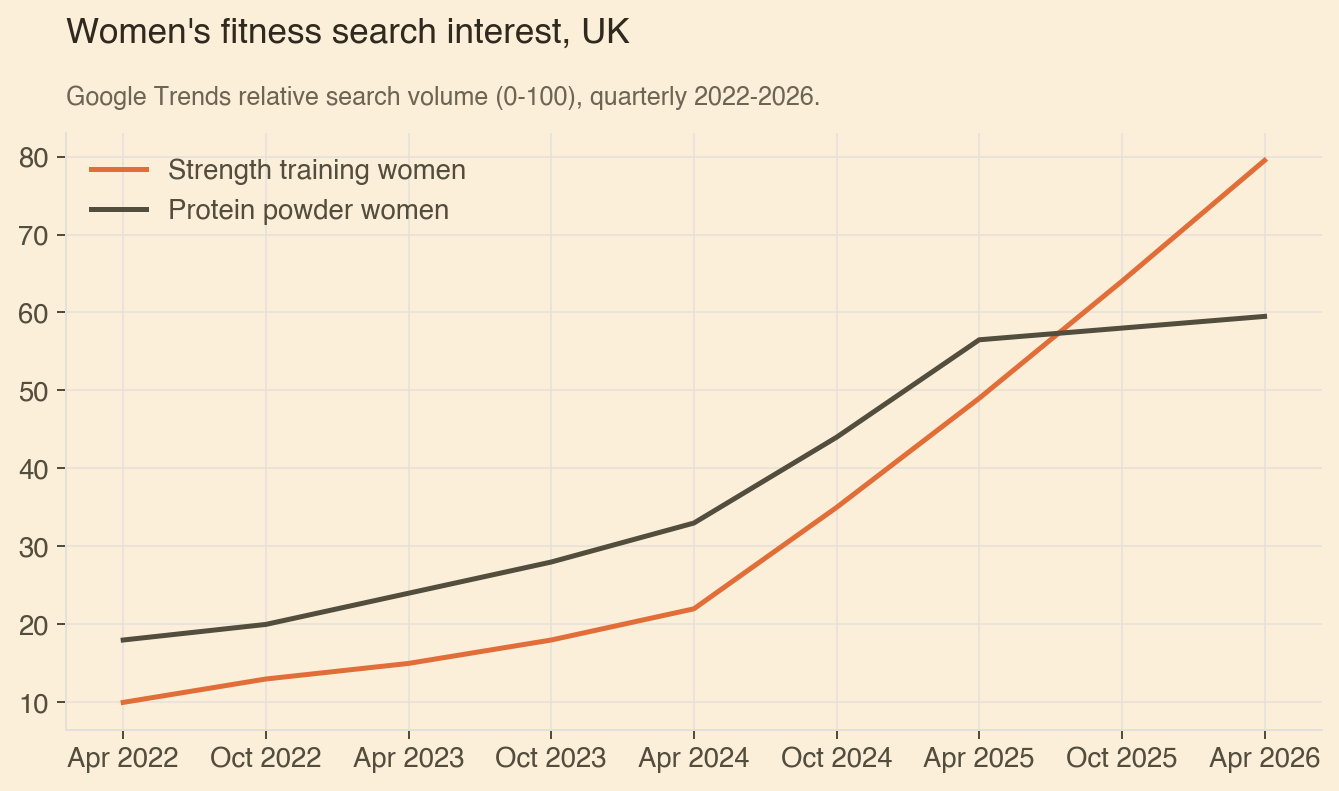

“Strength training women” searches are up 261% in two years, protein powder peaked

Google Trends data for “strength training women” shows a 62% increase year on year and a 261% increase over two years. “Protein powder women” is up 80% over that same two-year period. Gym membership searches are up 88% year on year. This isn’t a January resolution spike. The trend has been compounding for two years and it’s still accelerating. The UK women’s health supplements market is worth an estimated £1.18bn, growing at 5.7% a year.

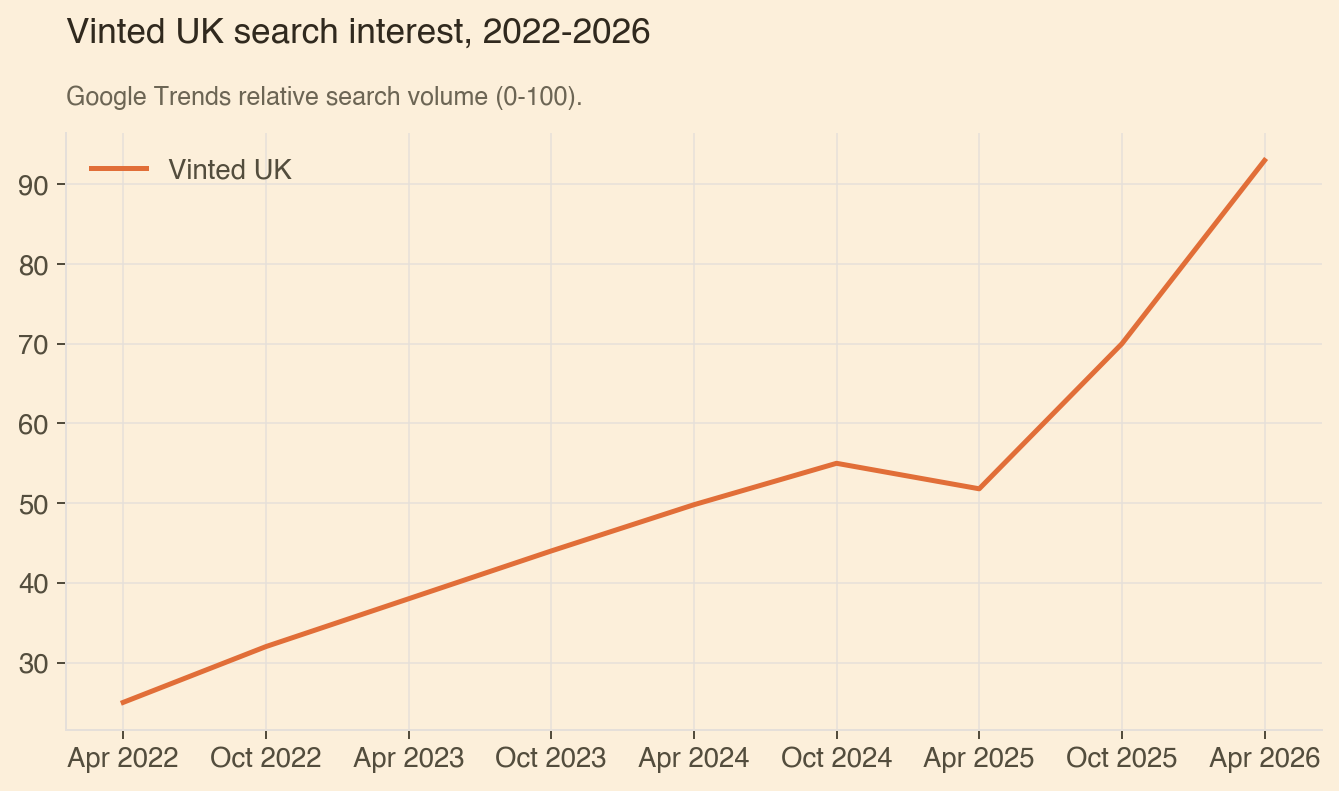

Vinted UK is up 80% and near all-time highs

“Vinted UK” sits at 93 out of 100 on Google Trends.

That’s up 80% year on year and 87% versus two years ago. It’s near the ceiling of search interest.

Meanwhile, ASOS reported sales down 9% globally and 5% in the UK in the first half of their financial year.

The secondhand market isn’t a niche. Every fashion DTC brand’s customer is now comparing prices against what they could get the same item for on Vinted.

The question isn’t whether resale competes with new. It’s whether “buy new” creative can make a convincing case.

Perimenopause is pulling health spending younger

Women as young as 33 are now spending on perimenopause solutions.

On r/AskWomenOver30, symptom management dominates the conversation: hot flushes during client meetings, brain fog at work, products that actually help.

The UK women’s health and beauty supplements market is valued at £1.18bn, growing at 5.7% a year.

Collagen supplements, a closely related category, are growing at 6.27%.

On Reddit, women describe buying fewer products but spending more per item, trading up to professional-grade solutions rather than adding more to the basket. That’s the pattern as people on these forums describe it, not confirmed market data, but it matches a market that’s growing in value faster than in volume.

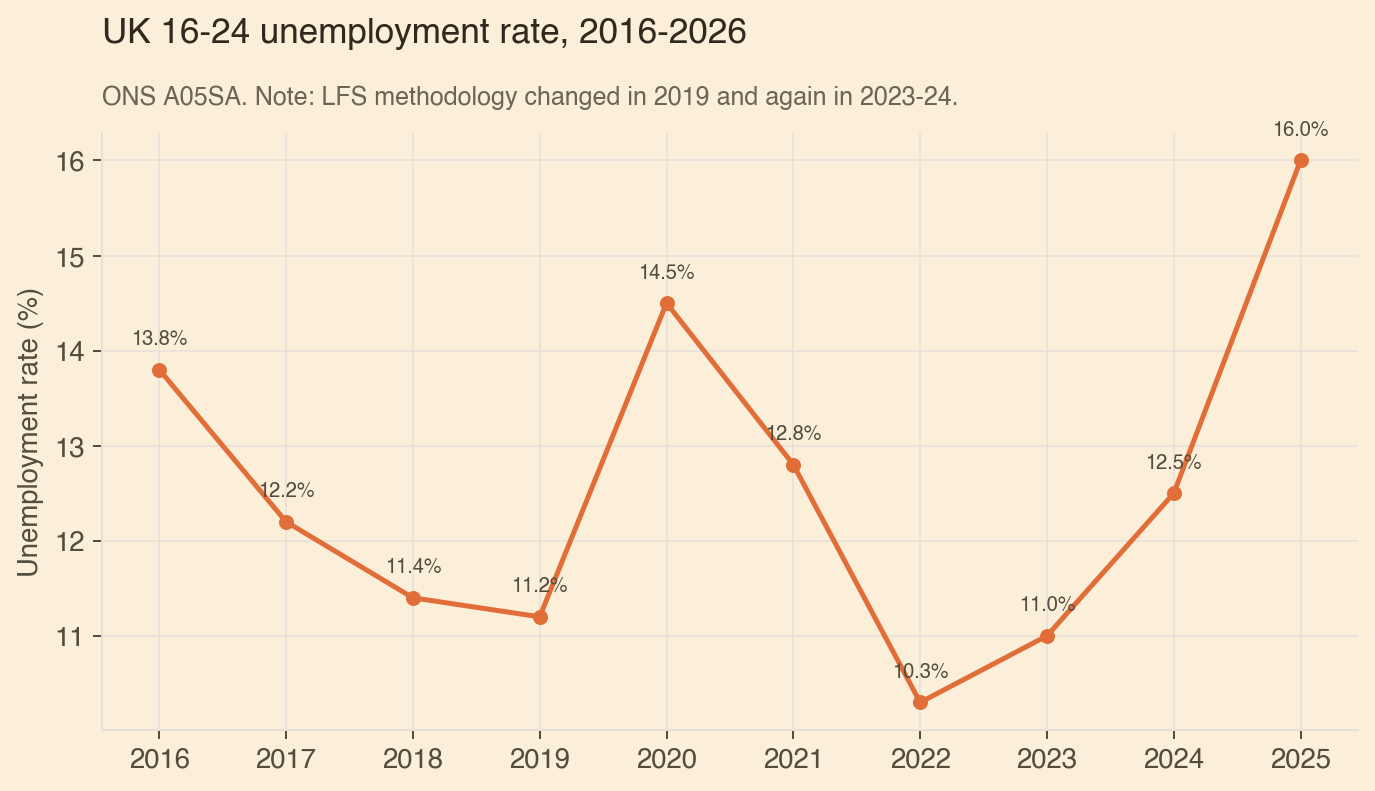

One in six UK 16-24 year olds is unemployed

The UK 16-24 unemployment rate hit 16.0% in the three months to January 2026.

That’s 731,700 people and the highest rate since 2014.

There are now 3 unemployed young people for every vacancy, up from 1.9 a year ago. The King’s Trust reports6 that seven in ten teenagers wish they weren’t starting their careers in this economic climate. For brands targeting Gen Z, the spending power simply isn’t there for a growing share of this age group.

Closing thoughts

None of this is a prediction. If I could call the next six months with confidence, I’d be running a hedge fund, not an agency.

But there does seem to be a vibe shift going on – even before the war began. There already seems to be anxiety about work, the future, and cost of living, and while these things have for the last few generations impacted those already worse off, today they’re hitting the higher earners.

AI might be intangible, but petrol hitting £2 will not be, or flight routes will not be.

People are still choosing to invest in themselves for now. Health continues to be an area of prioritisation, but done in the right way. It’s strength training and gym memberships over the continual escalation of supplements.

We know inherently how impactful these things are, but we’re not yet seeing it on the spending power. But short of a big shift in direction, I imagine we’re about to start seeing one in the months to come.

This has been fun to put together, and I look forward to reflecting at the start of July to see how right or wrong these things ended up being.

Have a great week

Josh

https://www.tuc.org.uk/news/tuc-calls-step-change-uk-approach-ai-poll-finds-majority-public-are-concerned-over-jobs

https://www.ofcom.org.uk/media-use-and-attitudes/online-habits/from-apps-to-ai-search-how-the-uk-goes-online-in-2025

https://fortune.com/article/price-of-oil-04-08-2026/

https://retailtimes.co.uk/worldpanel-by-numerator-grocery-inflation-holds-steady-as-shoppers-prepare-for-easter/

https://home.barclays/news/press-releases/20260/03/card-spending-grew-just-1-0-per-cent-in-february--while-inflation

https://www.kingstrust.org.uk/about-us/news-views/youthindex2025